KYC and Source of Funds for UK Racing Accounts: What Bookmakers Actually Check

Table of Contents

- Two processes the same operator runs — and why confusing them costs money

- Initial KYC at signup — what happens in the first hour

- Triggered SoF requests — when operators ask and why

- Acceptable documents — what cleans up an SoF request quickly

- Delays to free bet access — typical review timeframes

- Refusing to provide SoF — the consequences of declining the request

- Reader questions on identity and funding verification

Two processes the same operator runs — and why confusing them costs money

KYC and source-of-funds are often used as synonyms by punters and occasionally by customer-service staff who should know better. They are not the same process. Know Your Customer is the identity-verification framework every UK licensed operator runs at account opening to confirm who you are. Source of Funds is a separate compliance process, triggered by specific spending or deposit patterns, to confirm where the money funding your account came from. One happens at sign-up and is routine. The other happens when you have already been betting for a while and is typically a surprise. Confusing them leads to punters either under-preparing for the SoF trigger or over-panicking when the KYC request arrives.

The scale of these processes across the UK betting market is substantial. The Gambling Commission reported 3,086 active gambling licences as of 31 March 2025 — a decline of 2.3 per cent on the previous year, reflecting consolidation in the market — and the 24.4 million active remote betting and gaming accounts reported across those licences all represent KYC-verified relationships. Every new account opening triggers a KYC process; a smaller subset trigger ongoing SoF reviews across the customer lifecycle.

This piece walks through the initial KYC process at signup, the trigger conditions for a source-of-funds request, the documents operators typically accept, the delay this imposes on free bet access, and the consequences of refusing to provide SoF documentation.

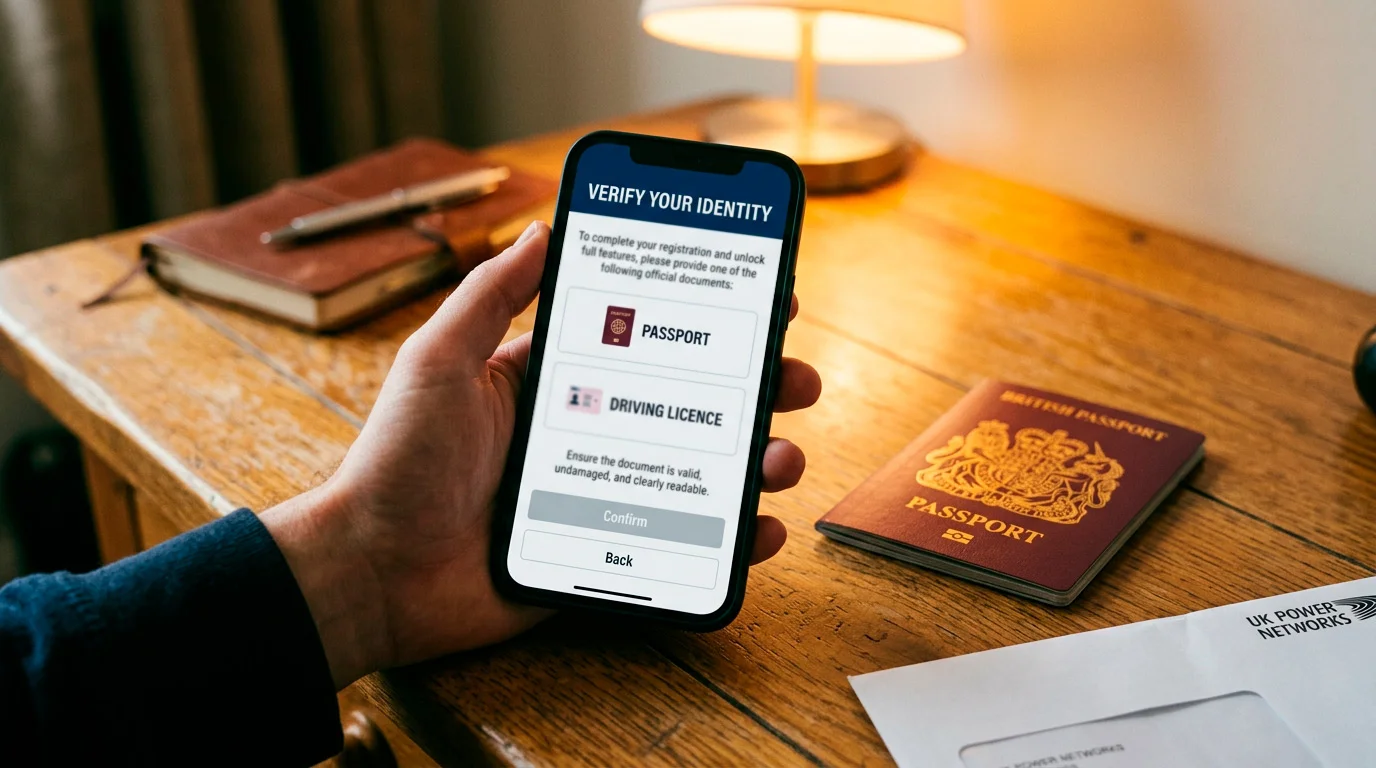

Initial KYC at signup — what happens in the first hour

KYC at account opening is the light-touch verification that confirms your identity matches what you have declared. The standard process runs automatically against electoral roll, credit file, and other publicly-available identity databases, and clears in seconds for most applicants. The information you supplied at registration — full name, date of birth, address, occasionally National Insurance number — is matched against those databases. A match clears you for initial account access; a failed match triggers a document upload request.

When the automatic match fails, the operator requests documentary evidence. Typical documents include a passport or UK driving licence for identity, and a utility bill, bank statement, or council tax bill for address. The document upload is reviewed by the operator’s KYC team — automatically at first, by a human reviewer if the automated check raises flags. Most document-based KYC clears within 24 to 72 hours of submission.

The interaction with promotional eligibility is important. Welcome offer free bet credits usually do not issue until KYC has cleared. A punter who places a qualifying stake before KYC clears may find the free bet credit delayed until the KYC review completes. At most operators the qualifying bet itself settles normally even if KYC is pending — the bet is accepted, the stake is taken, the outcome is settled at the market price. Only the promotional credit is gated behind KYC clearance.

Triggered SoF requests — when operators ask and why

Source of Funds is the separate process triggered later in the customer lifecycle. The triggers are not published by operators, but they cluster around specific patterns. Deposits exceeding a cumulative monthly threshold — typically £2,000 to £5,000 — will trigger SoF at most operators. A large one-off deposit of £5,000 or more will often trigger it regardless of cumulative monthly totals. Unusual deposit patterns that do not match the customer’s stated affordability — a £10,000 lump sum from a customer whose payslip evidence suggests a £30,000 annual salary — will trigger it.

The SoF process is more invasive than KYC. The operator is asking the customer to document where the money in their account came from, not just who they are. Documents commonly requested include recent payslips, tax returns for self-employed income, sale contracts for property or investment disposals, inheritance letters for gift or windfall funds, and dividend statements for portfolio-derived income. The operator is cross-referencing these against the deposit pattern in the account to confirm consistency between stated income and actual account funding.

The regulatory framework behind SoF is AML and anti-fraud. Licensed UK operators are obligated to satisfy themselves that customer funds are not proceeds of crime, and the SoF process is the primary operational mechanism by which this obligation is discharged. The process is not specific to gambling — it mirrors bank account SoF procedures — but the trigger thresholds in gambling are typically lower than in standard banking, reflecting the higher risk profile the regulator applies to the sector.

Acceptable documents — what cleans up an SoF request quickly

The documents that clear SoF review fastest are the ones that directly match the deposit pattern to a verifiable income source. A salaried customer depositing sums consistent with their net monthly take-home pay, providing three months of payslips plus a bank statement showing the salary hitting and the deposits leaving, clears quickly. The documents tell a coherent story that matches the account’s activity pattern.

Self-employed customers face more friction. Tax returns and company accounts are acceptable but require the operator’s reviewer to do more cross-referencing work, which lengthens the review cycle. Additional requests for invoice records, client-side confirmation of payments, or HMRC correspondence are not unusual for self-employed cases. The process is survivable but typically takes longer than for PAYE customers.

Windfall income — inheritances, property sales, investment disposals — requires its own specific documentation. An inheritance letter from the executor of an estate, a completion letter from a property sale, a dealing note from a broker for an investment disposal, all serve to evidence the one-off funds. These documents are typically straightforward to obtain but customers often do not have them filed for quick submission, which adds days to the process as the customer locates the paperwork.

Crypto-derived funds, gambling winnings from other operators, and cash-deposited funds are the categories that cause the most friction. Crypto requires wallet-address evidence and often a chain-of-custody analysis. Gambling-winnings-from-other-operators requires the other operator to provide confirmation of withdrawals — which they may be slow to do. Cash deposits with no clear audit trail may simply fail SoF review entirely, with the operator declining to accept the customer’s continued business.

Delays to free bet access — typical review timeframes

An SoF review imposes a freeze on account activity similar to the affordability review freeze. Deposits, stakes, and withdrawals are typically suspended pending review. Free bet credits are paused until the review clears. The customer experiences the SoF review as a period of account unavailability, typically lasting 48 hours to one or two weeks depending on the complexity of the case and the operator’s processing capacity.

The 72-hour target is the operator’s commonly-stated service-level for straightforward SoF cases. A PAYE customer with clean payslip-and-bank-statement documentation usually clears in that window. Cases requiring human reviewer attention, additional document requests, or consultation with compliance specialists can run materially longer — I have seen cases clear in three working days at one end and cases run for four weeks at the other.

The free bet implications are similar to the affordability-review case. Promotional credits in the account at the freeze point are typically preserved through the review and reissued or reinstated when it clears, with expiry periods restarted from the clearance date. Credits not yet issued at the freeze point are held in abeyance until the review resolves. Credits whose eligibility depended on completing specific qualifying activity during the freeze period are usually preserved with deadlines extended to account for the account-inactive period — but this is not universal, and punters with time-critical promotional positions should confirm the extension with customer service rather than assume it.

Refusing to provide SoF — the consequences of declining the request

The operator is required under its UKGC licence to satisfy itself on SoF where the risk profile requires it. A customer who refuses to provide requested documentation is effectively telling the operator the cross-reference cannot be completed, and the operator’s response is typically to close the account.

Account closure following SoF refusal returns the cash balance to the customer — subject to the operator’s ability to return the funds via the original deposit method — but forfeits any promotional credits not yet withdrawn. Free bet tokens, unwithdrawable bonus-balance funds, and pending promotional credits are typically lost in this scenario. The closure is reported to the customer with a reference code but usually without a detailed explanation, because the operator is not obligated to disclose the specific risk factors that drove the decision.

The closure does not necessarily propagate across operators. A customer closed at operator A for SoF refusal can often open an account at operator B and progress through KYC normally. However, the closure may register in shared industry databases under specific circumstances — particularly if the operator flagged the case as a suspected AML matter — and subsequent operator relationships may be complicated. In extreme cases, an SoF-refusal pattern across multiple operators can trigger referral to the NCA or other law-enforcement bodies. This is rare but not impossible. Which operators handle KYC and SoF reviews with the least friction — and which have reputations for heavy-handed freeze patterns — is one of the inputs I weigh in my piece on the best UK horse racing bookmakers.

Reader questions on identity and funding verification

How long does a UK bookmaker have to verify KYC after first deposit?

Under the current UKGC licensing framework, operators are required to complete KYC verification before a new customer places their first stake, not just their first deposit. This represents a tightening from the pre-2019 position when KYC could be completed post-first-bet. In practice most automatic KYC clears in seconds during the account-opening flow, with document-based verification completing within 24 to 72 hours for cases requiring manual review.

Can I withdraw free bet winnings before completing SoF checks?

No. An account frozen for SoF review typically has all withdrawal activity suspended until the review resolves. Free bet winnings sitting in the account balance at the freeze point are held alongside cash funds. When the review clears, withdrawals resume normally. If the review results in account closure, free bet winnings are forfeited while cash balances are returned to the original deposit method.

Created by the ”Free Horse Racing Betting” editorial team.